In the CJEU case of Mercedes Benz Financial Services (MBFS) the issue was whether certain supplies where of goods or services.

Technical Background

Before looking at the case, it is worthwhile considering the difference between goods and services and why the distinction is important. For most transactions the difference is clear, although sometimes (such as in this case) it is not immediately apparent. A starting point is that services are “something other than supplying goods”. Difficulties can arise in areas such as; provision of; information, software and, as MBFS discovered, Hire Purchase (HP)/leasing.

The distinction is important for two main reasons:

- VAT liability – Goods and services may have different VAT rates applicable

- Tax point – goods and services have different tax point rules, see here

The difference between HP and Leasing arrangements:

In an HP agreement the intention is usually for the ownership of the goods to pass when the final payment has been made. The transaction therefore relates to a supply of goods. If title to goods does not pass, this is leasing and represents a supply of services.

Case Background

MBFS offered certain contract purchases which were similar to many personal contract purchase deals for vehicles. These featured regular monthly payments with a final balloon payment. In the MBFS arrangements in question a significant difference to “usual” personal contract purchase agreements was that the balloon payment represented over 40% of the price of the car and payment of this fee was entirely optional.

The EU rules set out that there is a supply of goods where “in the normal course of events” ownership will pass at the latest upon payment of the final instalment. Consequently, the focus here was on whether the optional final payment meant that in the normal course of events the ownership of the car would pass to the customer.

Decision

The CJEU decided that the supplies were those of services rather than goods. This was based on the fact that, although the ownership transfer clause is an indicator of the transaction representing a supply of goods, there was a genuine economic alternative to the option being exercised. The circa 40% of the car price was a significant amount and it did not immediately follow that all customers would make this final payment. It was observed that in a “traditional” HP arrangement making the final payment was the “only economically rational choice”. This meant that the supply was one of services.

VAT Impact

As this was ruled to be a supply of services, output tax was not due from MBFS at the start of the contract (as would have been the case if the supply had been one of goods). This results in a significant cashflow saving.

Commentary

Any business which provides vehicles via HP or leasing arrangements should review its supplies and contracts to determine whether it can take advantage of this CJEU ruling. We are able to assist in this process.

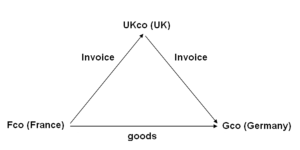

In this example; a UK company (UKco) receives an order from a customer in Germany (Gco). To fulfil the order the UK supplier orders goods from its supplier in France (Fco). The goods are delivered from France to Germany.

In this example; a UK company (UKco) receives an order from a customer in Germany (Gco). To fulfil the order the UK supplier orders goods from its supplier in France (Fco). The goods are delivered from France to Germany.