The Court of Justice of the European Union (CJEU) has released its decision in Brockenhurst College here

Unusually, it has gone against the Advocate General (AG) Kokott’s opinion (here) and concurs with previous decisions reached by the UK courts. This is good news for the taxpayer and other providers of educational services. The decision has been referred back to the Court of Appeal (CoA) for it to consider points such as the distortion of competition and the fulfilment of a separate function, however, it is likely that this will not affect the decision by the CJEU and HMRC’s appeal will be dismissed.

Background

The case considered two types of supply made by Brockenhurst College:

- The supplies made from its restaurant, used for training chefs, restaurant managers and hospitality students. The claim was made on the basis that these were exempt supplies of education and not standard rated supplies of catering

- Tickets for concerts and other live performances put on by students as part of their educational courses. These were similarly claimed to be exempt.

Students were enrolled in performing arts and catering and hospitality courses. As part of their course of study they were required to run a restaurant and stage live performances. Persons not enrolled on the relevant courses would pay for and attend these events. The services were usually supplied to a limited public including; parents, siblings, friends etc, and were supplied at a reduced cost as part of the practical element of the students’ education. The appellant argued that the experience was invaluable to their studies and should be regarded as ‘closely related’ to the principal supply of education. HMRC considered that the services in question were supplied to third parties in return for payment. Consequently, the services, whilst of benefit and practical experience to the students were separate VATable supplies made to third parties and the supplies cannot, therefore, be closely related to the supply of education to the student.

The First Tier Tribunal (FTT) concluded that the supplies in question were exempt as being closely linked to education because:

- the College was an eligible body and so its principal supplies were exempt supplies of education

- the supplies were integral and essential to those principal exempt supplies

- the supplies were made at less than their cost

- the supplies were not advertised to the general public. Instead, there was a database of local groups and individuals who might wish to attend the restaurant or performances

- the supplies were not intended to create an additional source of income for the College

HMRC disagreed with the conclusion on the basis that the supplies were outside the education exemption because the students were not the beneficiaries of the supplies in question, but only benefitted from making them. HMRC appealed to the Upper Tribunal (UT).

The UT rejected HMRC’s argument and agreed with the FTT. It held that the supplies were closely related to the exempt supplies of education because they enabled the students to enjoy better education. The requirement in the domestic law for the supplies to be for the direct use of the student was met because they were of direct benefit to him.

HMRC subsequently appealed to the CoA which referred it to the CJEU.

The AG’s opinion was that closely related transactions are to be regarded as independent supplies to the principal supply, but do not include the supply of restaurant or training services supplied to third parties who are not themselves receiving the principal supply of training. The third parties pay for their own consumption (of either the catering or performance) and do not pay for the provision of education. It is very rare that the CJEU makes a decision that goes against the AG’s opinion.

CJEU Decision

The CJEU ruled that activities consisting of students of a higher education establishment supplying, for consideration and as part of their education, restaurant and entertainment services to third parties, may be regarded as supplies closely related to the principal supply of education and accordingly be exempt from VAT – provided that those services are essential to the students’ education and that their basic purpose is not to obtain additional income for that establishment by carrying out transactions which are in direct competition with those of commercial enterprises liable for VAT, which it is for the national court to determine.

Action

We understand that there are a number of cases stood behind Brockenhurst. Any other colleges, FE, universities or other eligible bodies carrying out similar activities to Brockenhurst need to consider their tax position. It is possible that retrospective claims may be made, depending on specific circumstances. Treating such supplies as exempt may also impact on a body’s partial exemption position and could create business/non-business implications. This may also impact on activities like hairdressing, motor maintenance and beauty treatments which colleges provide on a similar basis to the activities in this instant case.

We are happy to discuss the implications of this case with you.

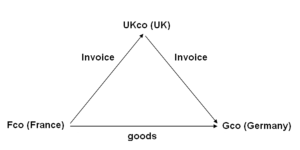

In this example; a UK company (UKco) receives an order from a customer in Germany (Gco). To fulfil the order the UK supplier orders goods from its supplier in France (Fco). The goods are delivered from France to Germany.

In this example; a UK company (UKco) receives an order from a customer in Germany (Gco). To fulfil the order the UK supplier orders goods from its supplier in France (Fco). The goods are delivered from France to Germany.