Investigation by The National Audit Office (NAO) into overseas sellers failing to charge VAT on online sales.

The NAO have investigated concerns that online sellers outside the EU are avoiding charging VAT. Full report here

The NAO has published the findings from its investigation into the concern that online sellers based outside the EU are not charging VAT on goods located in the UK when sold to UK customers. Online sales accounted for 14.5% of all UK retail sales in 2016, just over half of these were non-store sales, mainly through online marketplaces.

VAT rules require that all traders based outside the EU selling goods online to customers in the UK should charge VAT if their goods are already in the UK at the point of sale. In these cases, sellers should pay import VAT and customs duties when the goods are imported into the UK and charge their customers VAT on the final selling price. The sellers should also be registered with HMRC and are required to submit regular VAT returns.

Some of the key findings of the investigation are as follows:

HMRC estimates that online VAT fraud and error cost between £1 billion and £1.5 billion in lost tax revenue in 2015-16 but this estimate is subject to a high level of uncertainty. This estimate represents between 8% and 12% of the total VAT gap (The VAT gap is the difference between the amount of VAT that should, in theory, be collected by HMRC, against what is actually collected) of £12.2 billion in 2015-16. UK trader groups believe the problem is widespread, and that some of the biggest online sellers of particular products are not charging VAT. These estimates exclude wider impacts of this problem such as the distortion of the competitive market landscape.

HMRC recognised online VAT fraud and error as a priority in 2014, although the potential risk from online trading generally was raised before this. In 2013 the NAO reported that HMRC had not yet produced a comprehensive plan to react to the emerging threat to the VAT system posed by online trading. The report found HMRC had developed tools to identify internet-based traders and launched campaigns to encourage compliance but had shown less urgency in developing its operational response. Trader groups claim that online VAT fraud has been a problem as early as 2009, which has got significantly worse in the past five years. The Chartered Trading Standards Institute shares this view. Based on the emergence of the fulfilment house (a warehouse where goods can be stored before delivery to the customer) model, HMRC recognised online VAT fraud and error as one of its key risks in 2014 and began to increase resources in this area in 2015.

HMRC’s assessment is that online VAT losses are due to a range of non-compliant behaviours, but has not yet been able to assess how much is due to lack of awareness, error or deliberate fraud. Amazon and eBay consider that lack of awareness of the VAT rules is a major element of the problem. Amazon and eBay have focused on educating overseas sellers and providing tools to assist with VAT reporting and compliance. HMRC’s strategic threat assessment, carried out in 2014, concluded it was highly likely that both organised criminal groups based in the UK and overseas sellers in China were using fulfilment houses to facilitate the transit of undervalued or misclassified goods, or both, from China to the UK for sale online.

HMRC introduced new legal powers to tackle online VAT fraud and error in September 2016. The new joint and several liability power gives HMRC a new way to tackle suspected non-compliance, and is the first time any country has introduced such a power for this purpose. The new powers include making online marketplaces potentially jointly and severally liable for non-payment of VAT when HMRC has informed them of an issue with a seller, and they do not subsequently take appropriate action.

Conclusion

Online VAT fraud and error causes substantial losses to the UK Exchequer and undermines the competitiveness of UK businesses. Compliance with the VAT rules is a legal requirement. Not knowing about the rules does not excuse non-compliance. The UK trader groups who raised the issue report having experienced the impact of this problem through progressively fewer sales. They consider HMRC has been slow in reacting to the emerging problem of online VAT fraud and error and that there do not seem to be penalties of sufficient severity to act as a substantial deterrent.

It is too soon to conclude on the effectiveness and impact of HMRC’s new powers and whether the resources devoted by HMRC to using them match the scale of the problem. We recognise that HMRC must consider effort and efficiency in collecting VAT but its enforcement approach to online trade appears likely to continue the existing unfair advantage as perceived by UK trader groups. This is contrary to HMRC’s policy of encouraging voluntary compliance and it does not take account of the powerful effect that HMRC’s enforcement approach has on the operation of the online market as a whole. We intend to return to this subject in the future.

Further to the above, this article suggests that HMRC should have acted even earlier.

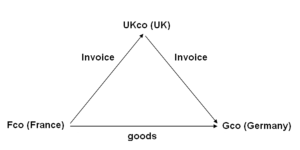

In this example; a UK company (UKco) receives an order from a customer in Germany (Gco). To fulfil the order the UK supplier orders goods from its supplier in France (Fco). The goods are delivered from France to Germany.

In this example; a UK company (UKco) receives an order from a customer in Germany (Gco). To fulfil the order the UK supplier orders goods from its supplier in France (Fco). The goods are delivered from France to Germany.